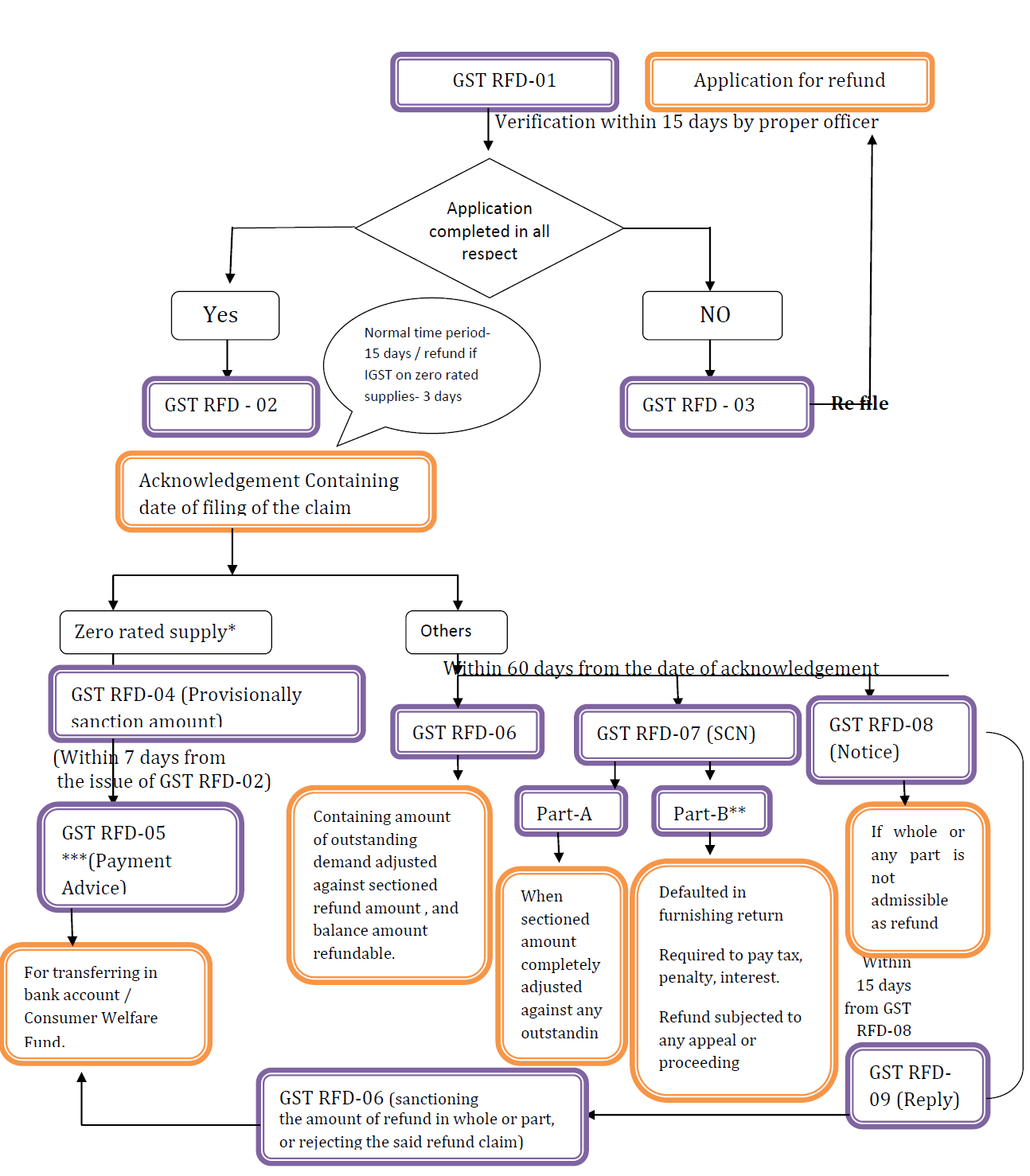

Process of Online refund under GST

The cash flow and working capital requirements of manufacturers and exporters could be adversely affected if a refund is delayed. As a result, one of the intentions of the implementation of GST is to ensure that the refund process is smoother so that manufacturers and exporters do not face issues due to delays. By ensuring that the refund process is facilitated quickly, tax administration becomes more effective.

The GST regime has provisions relating to refunds, and it aims at streamlining and standardising the procedures pertaining to refunds under GST. Therefore, a standardised form has been created to make claims for refunds. The procedure for making claims can be completed online in a timely manner.

* In case of zero rated supply the refund is made as following:

When the taxpayer claims refund of monies arising out of exports of goods or services, then an authorised officer can issue a provisional refund order in Form RFD-04 of an amount of 90% of the refund claim. Such a provisional refund can be made when the taxpayer:

- Has not been prosecuted for evading taxes for an amount exceeding Rs. 250 lakhs over a period of 5 years.

- Has a GST compliance rating of more than 5 out of 10.

- Has no appeal or review pending with respect to refunds.

Where the authorized officer feels that documents are in consonance with law, then he may pass a final order to that effect.

Time period for the provisional Refund : An order in FORM GST RFD-04 will be issued sanctioning the amount of provisional refund (90% ) within a period of 7 days from the date of issue of acknowledgement.

Final disbursement of refund amount must be made within 60 days . If the refund is not issued within 60 days, then the interest at the rate of 6% would be paid from the 61st day.

An payment advice in FORM GST RFD-05 will be issued by proper officer containing amount of provisional refund and money will transferred electronically in any of the bank account as specified in the application of refund.

**Refund can be withhold by the proper officer in the following conditions:

(1) Where the person claiming the refund has defaulted in furnishing any return,

(2) Where the person claiming the refund is required to pay any tax, interest or penalty, which has not been stayed by any court, Tribunal or Appellate Authority by the specified date.

Refund can be withhold by the commissioner in the following conditions:

Where refund order is subject to further proceeding or proceeding pending under any appeal, and the Commissioner is of the opinion that grant of such refund is likely to adversely affect the revenue in the said appeal.

Interest be paid for the holding refund claim which later on finalized in the favour of assessee. for which an order along with FOMR GST RFD-05 will be issued containing the following:

(a) Amount of refund which is delayed

(b) Period of delayed for which interest is payable,

(c) Amount of interest payable

*** If the claim qualifies for a refund, then an order shall be passed to that extent, or if it meets the criterion for being “unjustly enriching” the taxpayer, then the amount shall be transferred to the Consumer Welfare Fund.

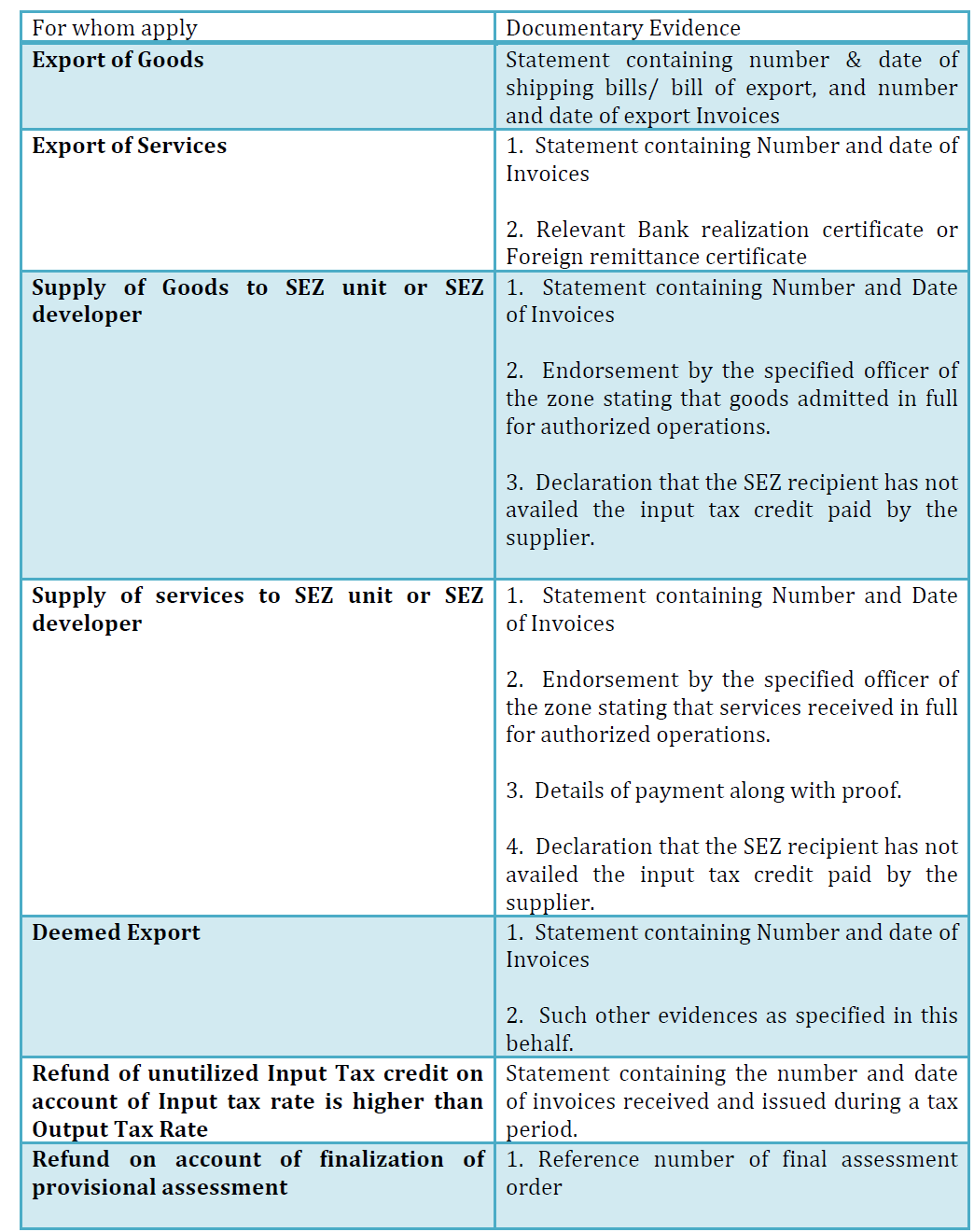

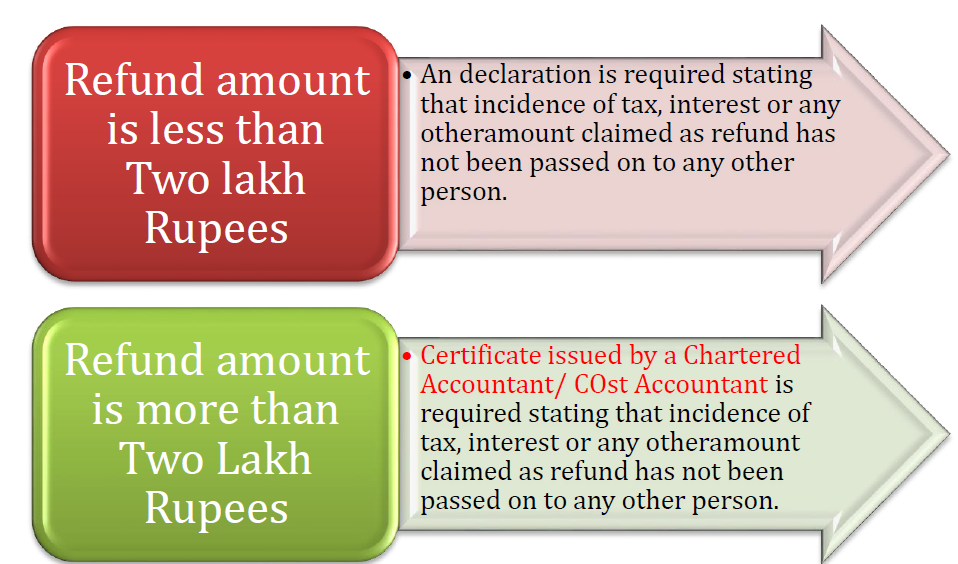

Documentary Evidence for refund

Certificate from Chartered Accountant/ Cost Accountant

Note: In the following cases no certificate/ declaration is not required to be issued:

1. Refund of tax paid on zero-rated supplies of goods or services or both or on inputs or input services used in making such zero-rated supplies.

2. Refund of unutilized Input Tax Credit at the end of Tax Period.

3. Refund of tax paid on a supply which is not provided, and for which invoice has not been issued, or where a refund voucher has been issued.

4. Refund of taxes paid on a transaction considered as Intra state supply (CGST & SGST) but subsequently held as Intra state (IGST).

5. Refund of taxes or interest paid by such class of persons as recommended by govt.

90% of refund of Integrated GST paid on export would be granted within 7 days and te balance within 60 days.

The GST refund would always arise in case of Export of Goods/services is done without submission of bond /LUT and IGST has been paid on exports.

In case the exports are done after submission of Bond/LUT, no IGST would be applicable. In such case, refund of Input Tax credit paid on expenses may arise.

The procedure and rules with respect to refund would be same as discussed, some additional points needs to be kept in mind, which are discussed as follows:

Export of goods and services or both without payment of IGST under bond or letter of undertaking

GST refund of Input Tax credit may arise in the following cases:

1. Input Tax credit unutilised when the goods/services supplied are zero rated or exempted from GST.

2. Were the input goods/services have a higher rate and output goods/services have a lower rate of tax.

3. In case of partial reverse charge, where the input tax credit can not be used completely against the output tax.

Refund Amount = Maximum admissible refund

Net ITC = Input tax credit availed on inputs and input services during the relevant period

Turnover of Zero Rated Supply of Goods = value of zero-rated supply of goods made during the relevant period without payment of tax under bond or letter of undertaking

Turnover of zero-rated supply of services = value of zero-rated supply of services made without payment of tax under bond or letter of undertaking

Value of zero rated supply of services = payments received during the relevant period for zero- rated supply of services

+ Zero rated supply of services during the relevant period for which advance received in prior period

– Advance received during relevant period for which services not given during the relevant period.

Adjustd Turnover = turnover in a State or a Union territory, as defined under clause (112) of section 2, excluding the value of exempt supplies other than zero-rated supplies, during the relevant period.

Relevant Period = Period for which claim has been filed.

- No refund shall be issued in case the refund amount is less than Rs. 1,000

- In case of refund due to casual taxable person or to non resident taxable person on account of advance tax deposited, such refund shall not be granted unless such person has not filed all returns for the entire period for which the certificate of registration was granted.

- UN Bodies and embassies can claim refund of the GST paid on their expenses within a period of 6 months, from the end of the quarter in which supply was received.

- Tourists can also claim a refund of the GST paid by them during their stay in India.

- Any claim for GST refund related to balance in Electronic cash ledger may be made through the return furnished for the relevant tax period in Form GSTR-3, GSTR-4, or FORM GSTR-7 .

- In cases where the application for GST refund related to refund of Input Tax Credit, the electronic cash ledger shall be debited by the applicant by an amount equal to the refund so claimed.

Seems cumbersome, don’t worry….

If you are having any query regarding GST refund process, please put your query on our portal www.efilingworld.com. Our team of experts will call you back and help to resolve your query.

Related Articles