Refund under GST

Timely refund mechanism is essential in tax administration, as it facilitates trade through the release of blocked funds for working capital, expansion and modernisation of existing business. The current tax structure is cumbersome, and it takes months and sometimes years to get refunds from the Government’s kitty.

GST provides for a clearer and efficient invoice based tracking system, verifying the transactions on an individual basis, thus, allowing systematic checking of the same. It comes as a huge relief for manufacturers or exporters, especially those in a 100% EOU or Special Economic Zone, whose working capital gets tied up in this cumbersome refund process.

The provisions pertaining to refund contained in the GST law aim to streamline and standardise the refund procedures under GST regime. Thus, under the GST regime, there will be a standardised form for making any claim for refunds.

The claim and sanctioning procedure will be completely online and time bound, which is a marked departure from the existing time consuming and cumbersome procedure.

What are the situations leading to Refund Claims ?

How to claim GST refund?

What is the time limit for claiming GST refund ?

How to calculate GST refund ?

Usually when the GST paid is more than the GST liability a situation of claiming GST refund arises. Under GST the process of claiming a refund is standardized to avoid confusion. The process is online and time limits have also been set for the same.

A claim for refund may arise on account of :

- Export of goods or services.

- Supplies to SEZs units and developers.

- Deemed exports

- Refund of taxes on purchase made by UN or embassies etc.

- Refund arising on account of judgment, decree, order or direction of the Appellate Authority, Appellate Tribunal or any court .

- Refund of accumulated Input Tax Credit on account of inverted duty structure.

- Finalisation of provisional assessment .

- Refund of pre-deposit.

- Excess payment due to mistake.

- Refunds to International tourists of GST paid on goods in India and carried abroad at the time of their departure from India.

- Refund on account of issuance of refund vouchers for taxes paid on advances against which, goods or services have not been supplied.

- Refund of CGST & SGST paid by treating the supply as intraState supply which is subsequently held as inter-State supply and vice versa.

Thus, practically every situation is covered. The GST law requires that every claim for refund is to be filed within 2 years from the relevant date.

Refund provisions for different persons

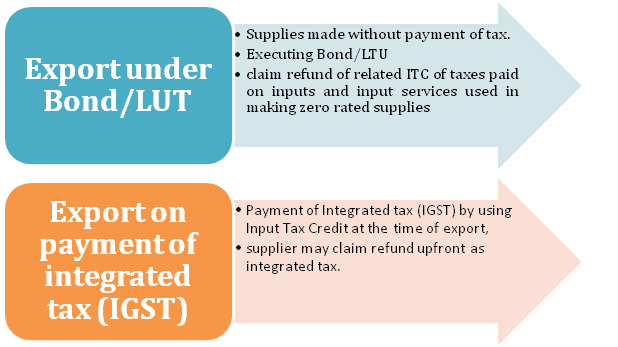

One of the major categories under which, claim for refund may arise would be, on account of exports. All exports (whether of goods or services) as well as supplies to SEZs have been categorised as Zero Rated Supplies in the IGST Act.

“Zero rated supply” under Section 16 of the IGST Act, 2017 means any of the following supplies of goods or services or both, namely:

(a) Export of goods or services or both; or

(b) supply of goods or services or both to a Special Economic Zone developer or a Special Economic Zone unit.

On account of zero rating of supplies, the supplier will be entitled to claim input tax credit in respect of goods or services or both used for such supplies even though they might be non-taxable or even exempt supplies.

Every person making claim of refund on account of zero rated supplies has two options.

Casual/Non-resident taxable person has to pay tax in advance at the time of registration. Refund may become due to such persons at the end of the registration period because the tax paid in advance may be more than the actual tax liability on the supplies made by them during the period of validity of registration period. The law envisages refund to such categories of taxable persons also. But the amount of excess advance tax shall not be refunded unless such person has filed all the returns due during the time their registration was effective. It is only after such compliance that refund will be granted.

Supplies made to UN bodies and embassies may be exempted from payment of GST as per international obligations. However, this exemption is being operationalized by way of a refund mechanism. So, a taxable person making supplies to such bodies would charge the tax due and remit the same to government account. However, the UN bodies and other entities notified under Section 55 of the CGST Act, 2017 can claim refund of the taxes paid by them on their purchases. The claim has to be made before the expiry of six months from the last day of the quarter in which such supply was received.

An enabling mechanism has been introduced in Section 15 of the IGST Act, 2017 whereby an international tourist procuring goods in India, may while leaving the country seek refund of integrated tax paid by them. The term, “tourist” has been defined and refers to any person who is not normally a resident of India and who enters India for a stay of not more than 6 months for legitimate non-immigrant purposes.

Further, Section 34 of the CGST Act, 2017 provides for issuance of credit notes for post supply discounts or if goods are returned back within a stipulated time. When such credit notes are issued, obviously it would call for reduction in output liability of the supplier. Hence, the taxes paid initially on the supply would be higher than what is actually payable. In such a scenario, the excess tax paid by the supplier needs to be refunded. However, instead of refunding it outright, it is sought to be adjusted after verifying the corresponding reduction in the input tax credit availed by the recipient. Section 43 of the CGST Act, 2017 provides for procedure for reduction in output liability on account of issuance of such credit notes. This is another form of refund by adjustments in the output tax liability. Such refund is not governed under the general refund provisions contained in Section 54 of the CGST Act, 2017.

The refund application has to be made in FORM RFD-1 within 2 years from relevant date.

The form should also be certified by a Chartered Accountant.

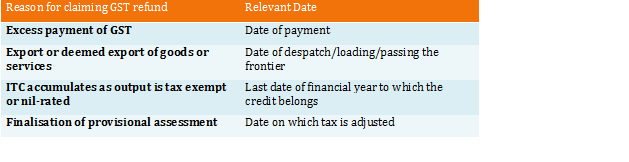

The time limit for claiming a refund is 2 years from relevant date.

The relevant date is different in every case.

Here are the relevant dates for some cases –

Also if refund is paid with delay an interest of 24% p.a. is payable by the government.

Let’s take a simple case of excess tax payment made.

Mr. A’s GST liability for the month of September is Rs 40000

But due to mistake, Mr. B made a GST payment of Rs 5 lakh.

Now Mr. B has made an excess GST payment of Rs 4.6 lakh which can be claimed as a refund by him.

The time limit for claiming the refund is 2 years from the date of payment.

If you are having any query regarding GST refund, please put your query on our portal www.efilingworld.com. Our team of experts will call you back and help to resolve your query.

[…] Refund under GST […]