All about Notice u/s 143 and how to give reply?

Many taxpayers have received notice under section 143(1)(a) after filing their Income-tax returns for AY 2017-18.

Now, it is important to understand that notice under section 143(1) and 143(1)(a) are two different notices and the way of dealing them is also different. So, one should not get confused between the two.

What is notice under section 143(1)(a)?

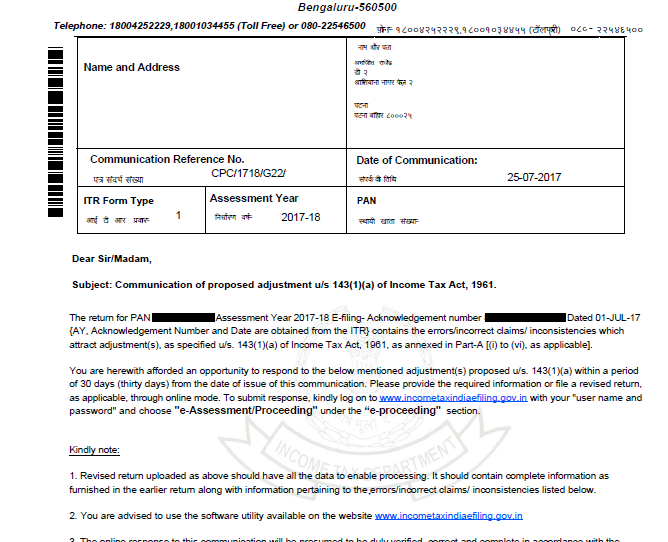

Notice u/s 143(1)(a) is an intimation from the Central Processing Centre (CPC) seeking clarification of the mismatch between the Income and deduction when compared to Form 16, Form 16A or Form 26AS.

What is the time period for sending a response towards this notice?

A time period of 30 days from the date of receiving the intimation is given to the recipient of the notice. If the recipient fails to respond, the return is processed after making necessary adjustment(s) u/s 143(1)(a), without providing any further opportunities in this matter.

How to deal with the notice under section 143(1)(a)?

Step 1:

Take a look at the page 2 of the notice received. This page will help you understand the reason why this notice is issued to you and you can know the exact difference.

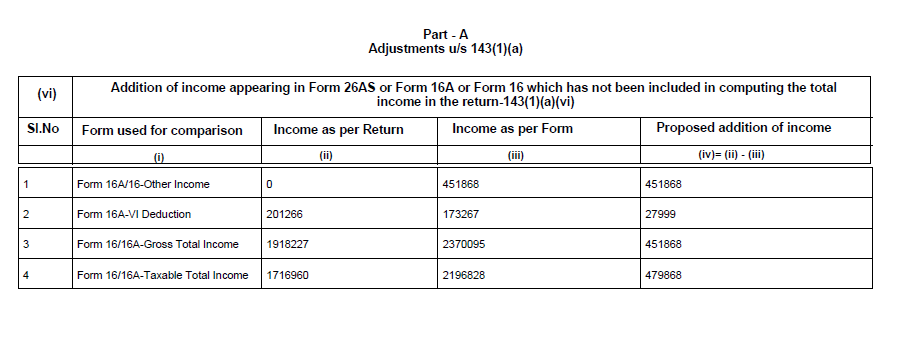

In the example case given above, the reason of difference is that the assessee has not declared his “Other Income” of Rs.451868 in his return, whereas this income is being displayed either in his Form 26AS or Form-16 or Form-16A.

It is important to note that the details entered in the Income-tax return should match with Form-16, Form-26AS and Form-16A, if any.

The second reason of difference in the given case is of Deductions u/s Chapter VIA. If you have claimed some deductions which are not included in your form 16, then also, you may receive this notice.

Step 2:

After understanding the difference, take the required action as below (this is basis above example case which is most common one. Some cases may differ and its required action).

- Declare the Other Income in the revised return and,

- Regarding deductions, if you have the proofs of deductions, then simply attach the same while responding to this notice (steps explained below). However, if you do not have the deduction proofs, then you cannot claim those deductions which are not displayed or not considered in your Form-16.

Procedure to Respond for notice u/s 143(1)(a)

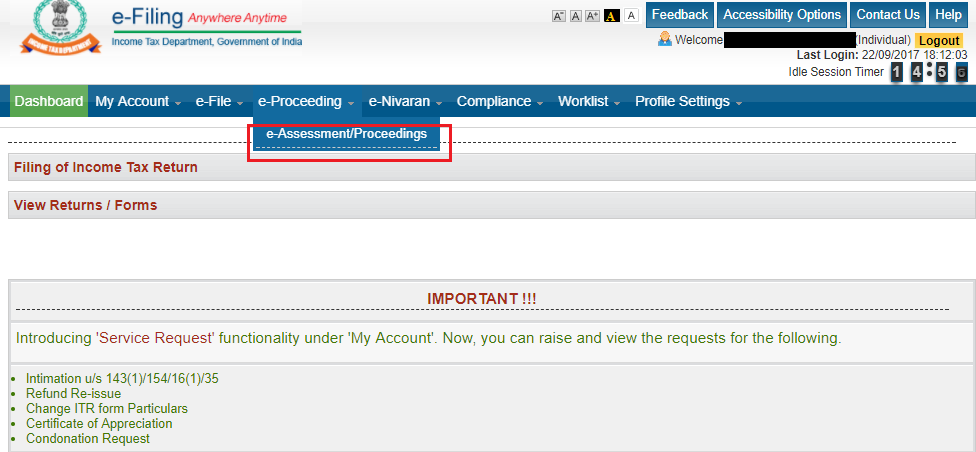

Log in to Income-tax Department website www.incometaxindiaefiling.gov.in

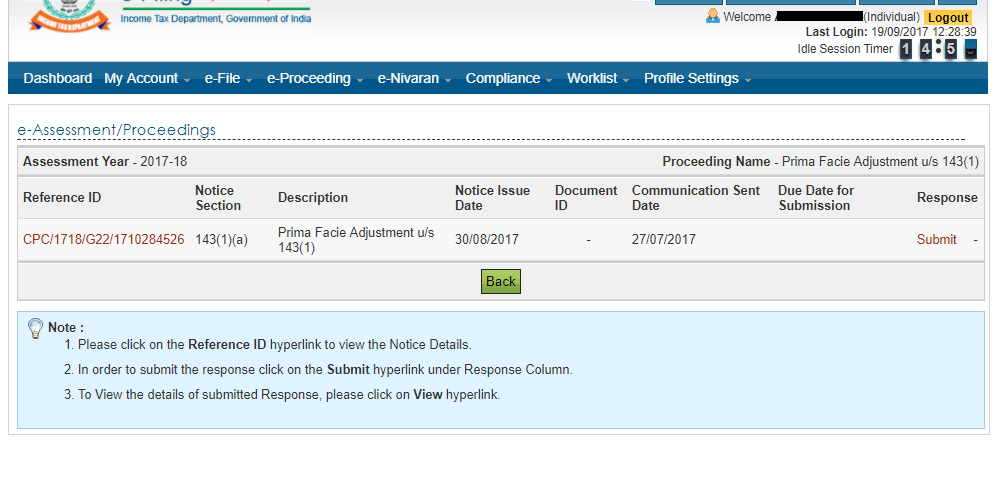

Go to ‘e-Proceeding’ menu option and further choose ‘e-Assessment/Proceedings’ as shown below:

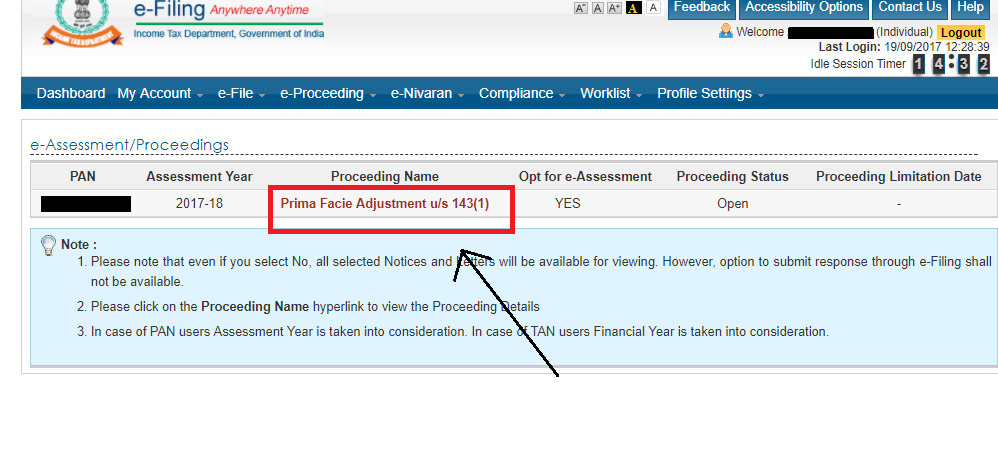

After clicking on “e-Proceeding”, you will see a screen as given below. Click on ‘Prima Facie Adjustment u/s 143(1)(a)’.

4. After that, the following screen will be displayed. Click on Reference ID

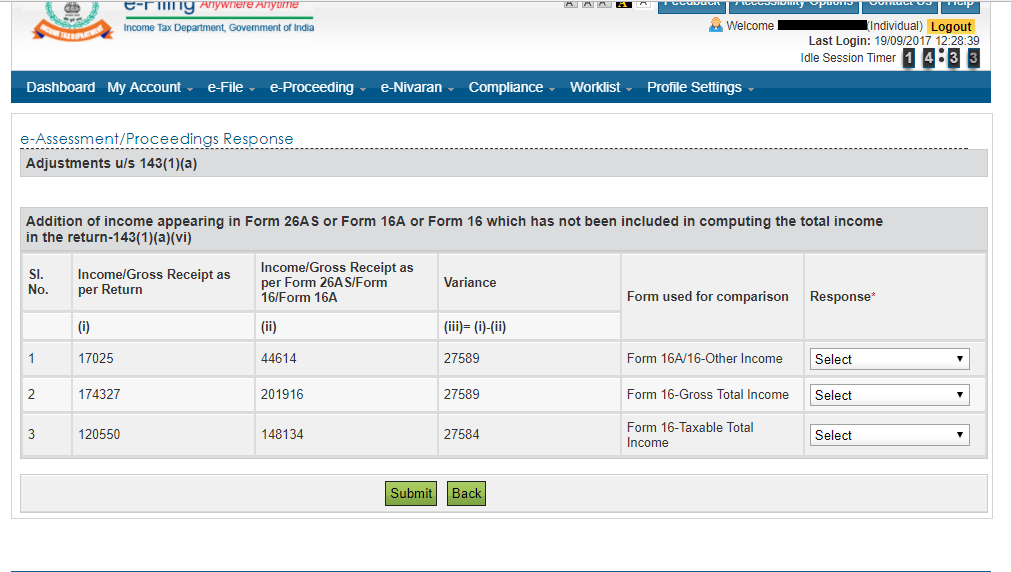

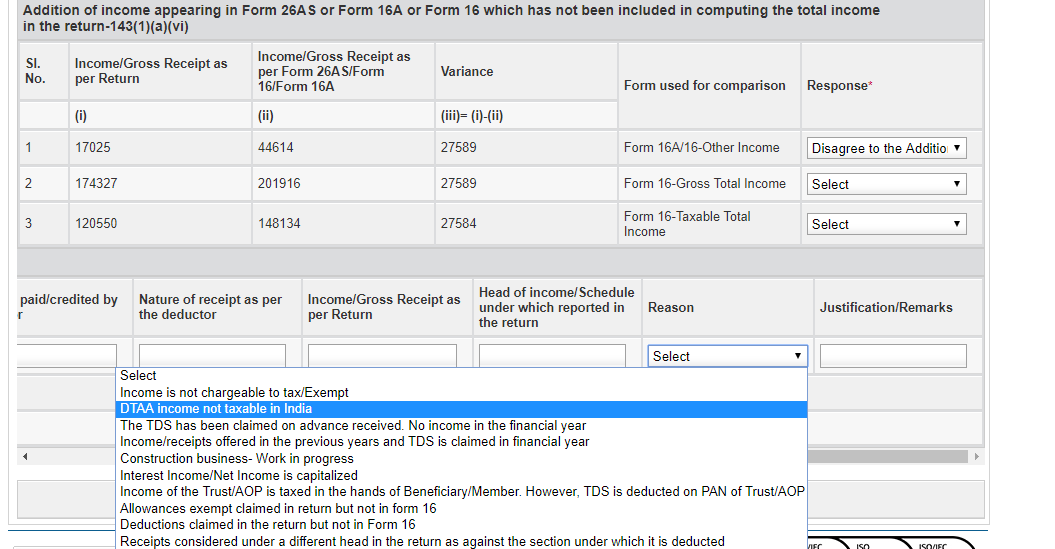

5. You will see the response screen as shown below:

6. Now you have to select whether you ‘Agree’ or ‘Disagree’ with the adjustments in the notice and accordingly you have to select the same from the Drop-down.

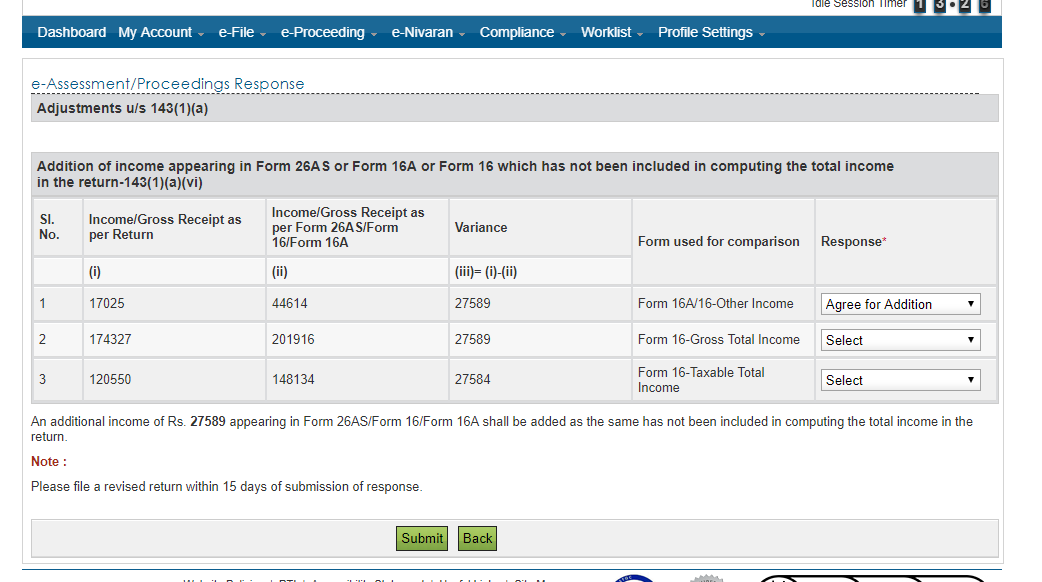

If you Agree for addition, you will have to make the relevant adjustments and modifications in the return and revise it and also pay the additional tax amount, if any.

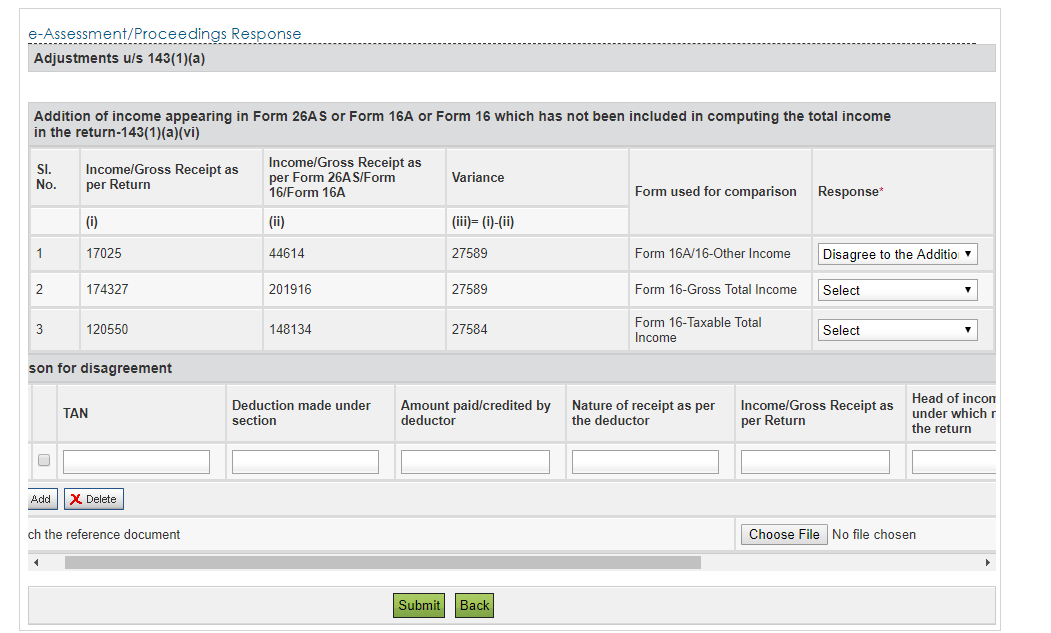

If you Disagree with the adjustments, you will find a box open up, where you will have to enter the reason for disagreement and also attach supporting documents before you submit your response.

You need to enter:

- TAN – This is the TAN of the employer which is available in Form-16 / Form16-A / 26AS copy.

- Deduction made under section – You need to enter section 192, if you have made a deduction against Salary Income. If deduction is not made under Salary Income, you can directly enter the section of deduction claimed.

- Amount paid/credited by deductor – Check your Part-A of Form-16 to find this amount.

- Income / Gross Receipt as per return – Enter the Income after taking the deductions into account.

- Head of Income / Schedule under which reported in the return – Enter the relevant head of Income in question here.

- Reason – While selecting the reason, you will see a list as shown below. Select the relevant reason from the drop-down. Select the reason diligently.

Justification Remarks – You can mention any specific remarks regarding your Income or deductions in question in this column. Once you have entered these details, you need to attach the supporting proofs relating to discrepancy addressed, for eg- 80C, 80D proofs, rent receipts, etc.

Lastly, just click on “Submit” button and an ‘Acknowledgement’ of your response being submitted shall be displayed.

Do not forget to revise the return if you have agreed to the adjustments in the notice.

What is the time limit to revise the return in this case?

If you have opted to file revised return, then you must file a revised return within 15 days.

Important Note – Sometimes, filing of response to the notice of Income-tax Department may become a tedious task for the assessee (tax payer). Therefore we have started a new service for our users called Notice Assistance where our tax experts will help resolve the notice received in best possible way.

In case of any query regarding Notices issued u/s 143(1) or for filing your Income Tax Return, plz leave your query on www.efilingworld.com or call us at +91-8279436547.