Tax Deducted on Source (TDS) Under GST @2% (With Examples)

TDS @ 2% is required to be deducted on payment made to the supplier of goods and services where contracted value exceeds Rs. 2.5 Lakh.

TDS Provisions are effective from 01st Oct, 2018 via Notification No. 50/2018-Central Tax dated 13th Sep 2018.

Section 51 of CGST Act, 2017 provides the provision of Tax deducted at Source under GST.

Persons required to deduct TDS under GST

The following person are required to deduct TDS under GST:

- A department or establishment of the Central Government or State Government; or

- local authority; or

- Governmental agencies; or

- such persons or category of persons notified by the Government

The government has also notified the following mentioned person which are required to deduct the TDS under GST:

- An authority or a board or any other body, with fifty-one per cent. or more participation by way of equity or control, to carry out any function-

a.Set up by an Act of Parliament or a State Legislature; or

b. Established by any Government,

2. Society established by the Central Government or the State Government or a Local Authority under the Societies Registration Act, 1860 (21 of 1860)

3. Public sector undertakings.

Persons not mentioned above need not to deduct TDS under GST.

Criteria for TDS Under GST

TDS is to be deducted where contracted value exceeds Rs. 2.5 Lakh, while checking contracted value, following needs to be excluded:

- Central Tax,

- State Tax,

- Union Territory Tax,

- Integrated Tax,

- Cess

Calculation of TDS @2% or 1% ?

In case of intra state supply, TDS needs to be deducted @1% under CGST and SGST both, i.e. 2%, while in case of inter state supply, TDS is to be deducted @ 2% as IGST.

While calculating TDS in GST, all the taxes mentioned in Invoice needs to be excluded.

Example:

Mr. A supplies goods to Mr. B within the same state under a contract of Rs. 5 Lakh, where CGST @9% and SGST @ 9% is levied. While making payment of Rs. 5 Lakh, Mr. B shall deduct TDS of Rs. 1% of Rs. 5 Lakh under CGST and Rs. 1% of Rs. 5 Lakh under SGST and rest Rs. 4,90,000 will be paid to Mr. A. The value for TDS purpose shall not include 18% GST.

In case if supply is made to different state i,e, Inter State Supply, IGST of Rs. 10,000 to be deducted as TDS.

Scenarios under which no TDS is to be deducted

- If the contracted value is less than Rs. 2.5 Lakh, no TDS is required to be deducted, lets understand it with the help of some examples:

a. A enters into a contract of Rs. 1.5 Lakh, in this case no provision of TDS will be applicable.

b. A enters in to a contract of Rs. 3.5 Lakh, where he receives payment of Rs. 1.5 Lakh in advance and rest Rs. 2 Lakh at a later date, in this case provision of TDS will be applicable because contracted value exceeds by Rs. 2.5 Lakh.

c. A enters into an contracts of Income Tax Advisory of Rs. 1.5 Lakh also into an another contract of Rs. 2.00 Lakh for GST advisory, in this case provision of TDS will not be applicable as there are two contracts and both are having value less than Rs. 2.50 Lakh.

Hence, we can say that for applicability of TDS emphasis is towards contracted value only.

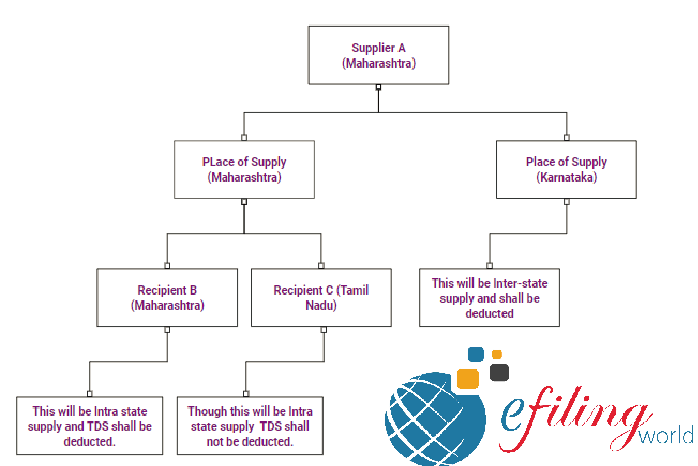

- Where the place of recipient is different from place of supplier and place of supply. Lets understand it with help of some examples:

- A enters in a contract with ABC Ltd., both are having there registered office at Maharashtra. It would be intra state supply and TDS (Central plus State Tax) shall be deducted. It would be possible for Mr. A( Supplier) to take credit of TDS in his electronic credit ledger.

- Supplier as well as place of supply are in different states. In such cases, integrated tax would be levied. TDS to be deducted would be TDS (Integrated tax) and it would be possible for the supplier (i.e. the deductee) to take credit of TDS in his electronic cash ledger.

- Harayana government enters in a contract with Hotel Taj Mumbai (Maharashtra) for Rs. 6 Lacs, to rent space for conducting an seminar, in this case Hotel Taj will levy CGST and SGST, Maharashtra. Here,

- Place of Supply- Maharashtra

- Location of Supplier- Maharashtra

- Location of Recipient- Harayana

No TDS provisions will be applicable in this case irrespective of contracted value, as place of supply and supplier is different from the location of recipient.

In this case, the supply would be intra-State supply and Central tax and State tax would be levied. In such case, transfer of TDS (Central tax + State tax Maharashtra) to the cash ledger of the supplier (Central tax + State tax Harayana) would be difficult. So in such cases, TDS would not be deducted.

Therefore, while determining the applicability of TDS on GST its very important to determine the place of supply.

We can also understand above mentioned scenarios with the help of following diagram:

Registration of TDS Deductor

The TDS deductor has to compulsorily register under GST irrespective of threshold limit.

A TDS deductor can obtain GST registration using his Tax deduction and collection Account Number (TAN) issued under the Income Tax Act, 1961. Its not mandatory to have Permanent Account Number (PAN) for him for GST registration.

Deposit of GST TDS with government and issuance of TDS certificate

TDS should be deposited with the government by dedcutor (recipient) by 10th of the next month of TDS deduction in form GSTR-7 through the GST online portal-www.gst.gov.in. The deductor would be liable to pay interest if TDS deducted is not deposited within the prescribed limit as mentioned above.

A TDS Certificate is required to be issued by TDS deductor (the person who is deducting the TDS) in Form GSTR-7A to the deductee (whose TDS has been deducted) within 5 days from the date of depositing the TDS to the government.

If the TDS deductor does not issue the TDS certificate to the Deductee within the aforementioned time limit, he would be liable to pay late fees of Rs. 100/- per day from the date of expiry of 5th day till the certificate is issued. However, this late fees would not more than Rs. 5000/-.

The TDS detailes furnished by the. TDS deductor will be reflected in GSTR 2A of dedcutee (Supplier) and the supplier may include and avail the same in GSTR-2. The supplier can take this amount as credit in his electronic cash register and use the same for payment of tax or any other liability.

Penalty for not complying with provisions of TDS in GST

| S. No. | Event | Consequence |

| 1 | TDS not deducted | Interest to be paid along with the TDS amount; else the amount shall be deter mined and recovered as per the law. |

| 2 | TDS certificate not issued or delayed beyond the prescribed period of five days | Late fee of Rs. 100/- per day subject to a maximum of Rs. 5000/- |

| 3 | TDS deducted but not paid to the government or paid later than 10th of the succeeding month | Interest to be paid along with the TDS amount; else the amount shall be determined and recovered as per the law. |

| 4 | Late filing of TDS returns | Late fee of Rs. 100/- for every day during which such failure continues subject to a maximum amount of five thousand rupees. |

Any excess or erroneous amount deducted and paid to the government account shall be dealt for refund under section 54 of the CGST Act, 2017. However, if the deducted amount is already credited to the electronic cash ledger of the supplier, the same shall not be refunded.

The author of this article is CA Arti Agarwal. She is a practicing Chartered Accountant and also a prominent author of efiing world.