Computation of Short Term & Long Term Capital Gain on sale of property

Capital Gain tax on property

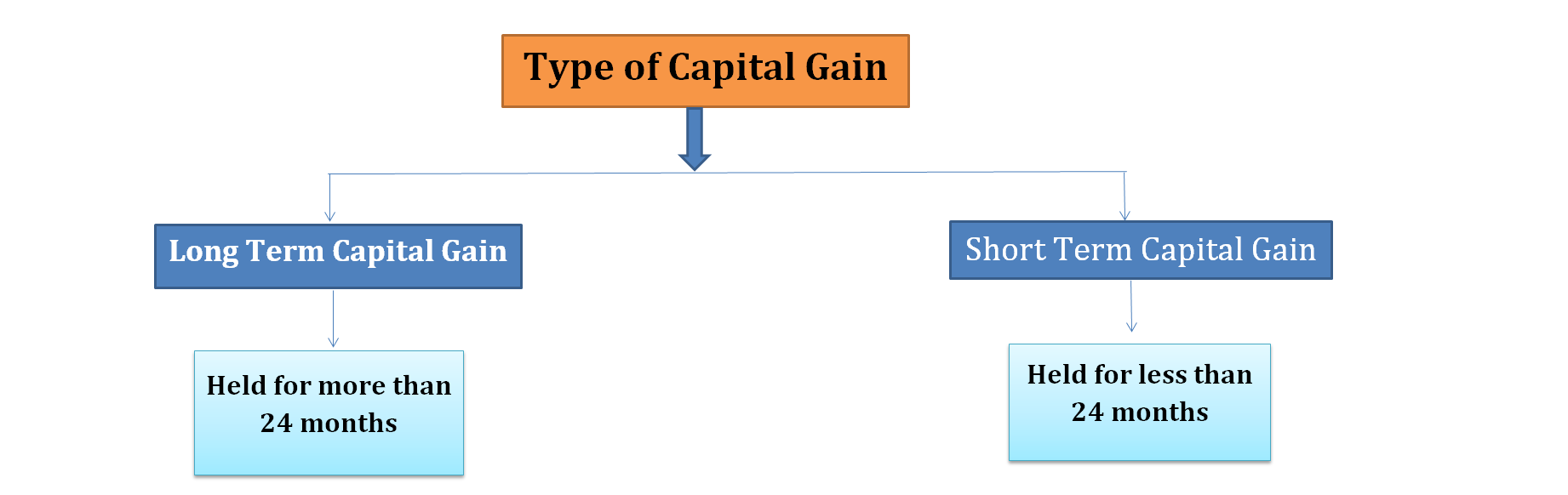

Any gain or loss arises on sale of a capital assets is termed as Capital Gain. Since, real estate is a capital assets, hence, If we sale any real state property, capital gain arises. It may be long term capital gain or short term capital gain under Income Tax. Classification of the capital gain as per income tax is as follows:

- Short Term Capital Gain: If property being sold is held for less than 24 months, it will be treated as short term capital gain.

- Long Term Capital Gain: If property being sold is held for more than 24 months, it will be treated as long term capital gain (Reduced from 36 months to 24 months from FY 2017-18 onwards).

It is important to note that the gain arises on the sale of property is classified under the head “Income from Other Sources”, but the income arises from renting the property is being show under the head “Income from House Property” and taxed accordingly.

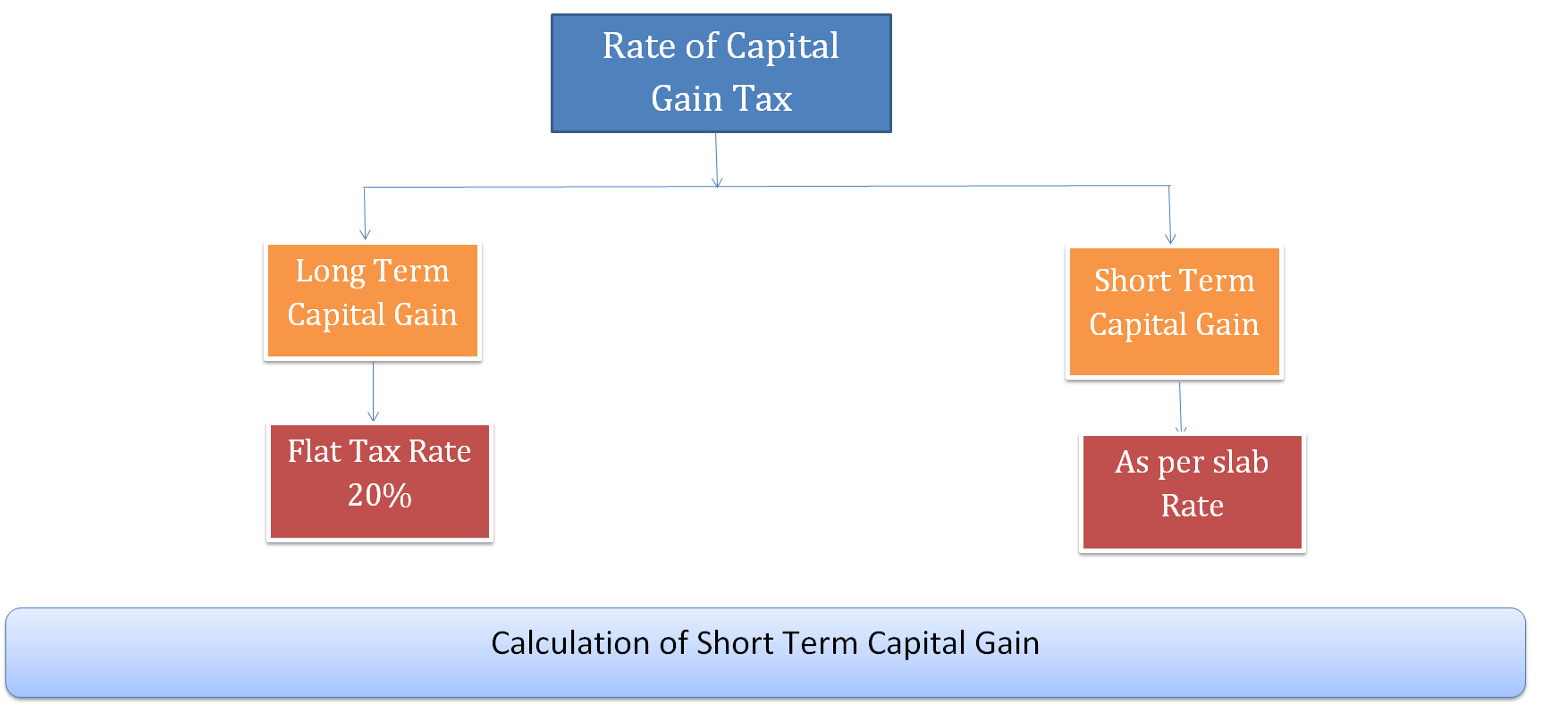

Capital Gain tax Rate on short term and long term capital gain

| Particulars | Tax Rate |

| Short Term Capital Gain | As per Normal Income Tax Slab |

| Long Term Capital Gain | 20% |

In case short term capital gain arises, computation is to be done as follows:

| Full Value of consideration | xxx | |

| (Less) | Expenditure incurred wholly and exclusively in connection with such transfer/sale | xxx |

| (Less) | Cost of Acquisition | xxx |

| (Less) | Cost of Improvement | xxx |

| Gross Short Term capital Gain | xxx | |

| (Less) | Exemption (If any) available u/s 54B/54D/54G/54GA | xxx |

| Net Short Term Capital Gain on sale of property | xxx |

Tax is to be calculated short term capital gain as per normal tax slab.

If long term capital gain arises, on sale of real estate property, calculation is done in the following manner:

| Full Value of consideration | Xxx | |

| (Less) | Expenditure incurred wholly and exclusively in connection with such transfer/sale | Xxx |

| (Less) | Indexed Cost of Acquisition | Xxx |

| (Less) | Indexed Cost of Improvement | Xxx |

| Gross Long Term capital Gain | Xxx | |

| (Less) | Exemption (If any) available u/s 54B/54D/54G/54GA | Xxx |

| Net Long Term Capital Gain on sale of property | Xxx |

Tax @20% shall be payable on the long term Capital Gain computed above and advance tax shall also be liable to be paid on such capital gain.

The difference between calculation of LTCG and STCG is in calculation of LTCG cost is indexed for adjustment of inflation, so when we calculate LTCG by considering Index cost of acquisition and cost of improvement, it reduces the amount of capital gain. But this benefit is not available in case of short term capital gain.

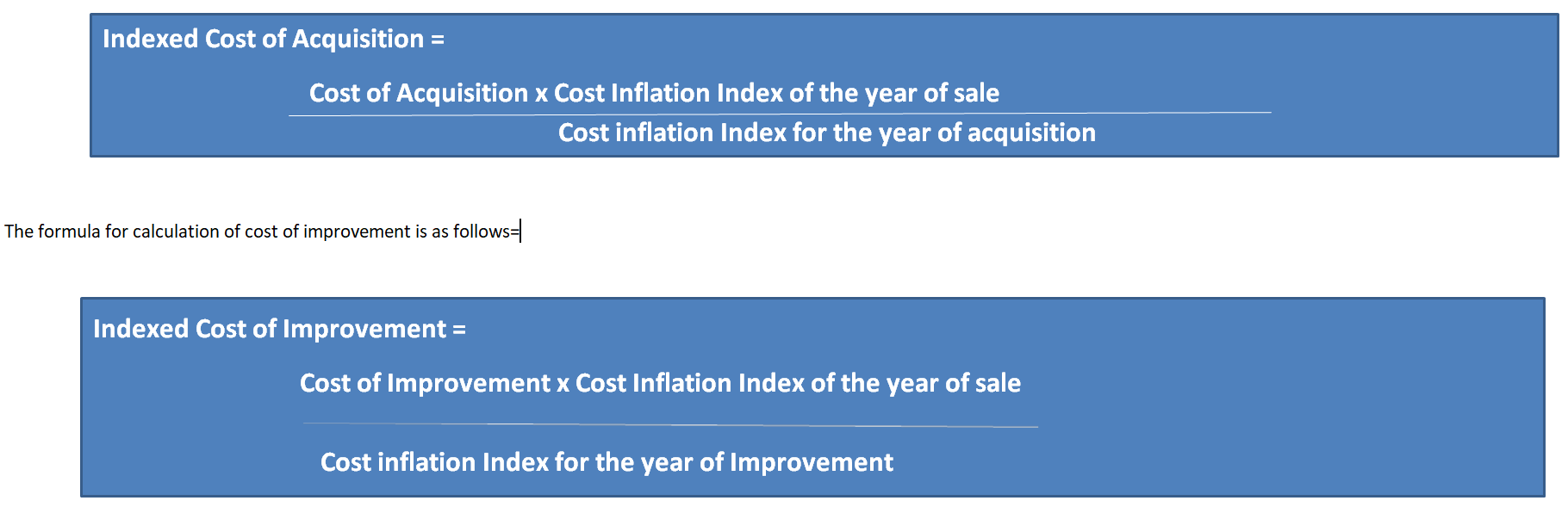

Meaning of Indexation

Indexation refers to the process by which the cost of acquisition is adjusted for the inflationary rise in the value of the asset. For this purpose, the government has released cost inflation index, which is updated every year so as to account for the inflation of that year.

For the purpose of computation of indexation the following details are required:

- Year of Acquisition/ Improvement

- Year of Transfer

- Cost of Acquisition/ Improvement

- Cost Inflation Index for the year of Acquisition/ Improvement

- Cost Inflation Index for the year of sale

The formula for calculation of cost of acquisition is as follows =

The Author of this article is CA Arti Agarwal. She is a practicing Chartered Accountant and also a prominent writer of Efiling World. If you are having any query regarding Capital Gain then you can send your queries at info@efilingworld.com , also you can contact on +91-8126416416.