ITC Rules for Common Credit under GST

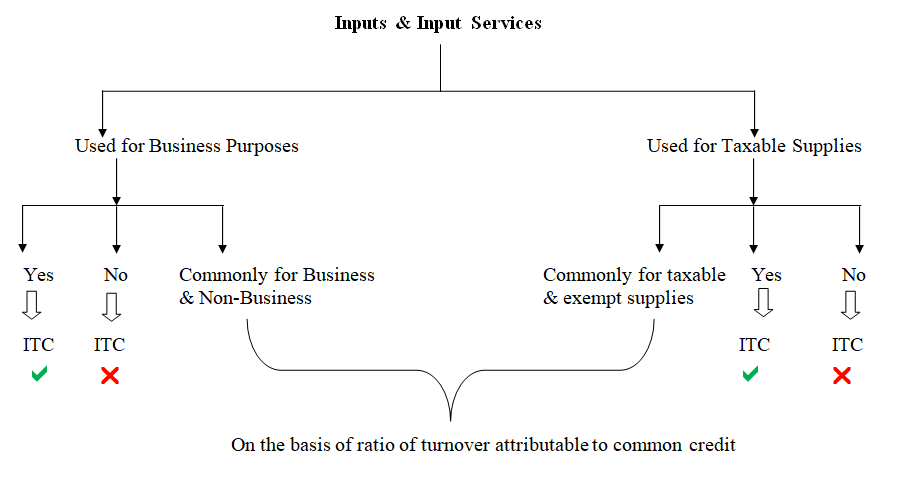

Many of the businesses use same services and goods commonly for business and personal purpose, simultaneously same inputs are commonly used for providing taxable as well as non-taxable goods.

But ITC is only available on those inputs which are used for business purpose and for taxable supply. Let’s understand with the help of following example:

Mr. Vihaan Gupta is a whole sale trader. He has taken a two- story building and uses the ground floor for commercial purpose and first floor for residential purpose. There is also a plot adjacent to the building where he grows vegetables and sells them in his shop.

Now, in the above case same property is used for three different purposes, for taxable supplies (Shop), exempt supply (Vegetable) and for personal (residence).

As per law, ITC is available only for business purpose and taxable supplies and not for personal purpose and non-taxable supplies.

Mr. Vihaan Gupta is eligible for GST paid on the business expenses but there are some expenses like rent which are commonly used for business and personal purpose. Hence GST on rent (rent paid for commercial purpose) is the common credit.

Why is it important to understand the concept of common credit?

ITC is only available for inputs used for business purpose; hence if there are some business expenses which are incurred for business and personal purpose both, we will have to reverse that portion of business expenses which are used for personal expenses.

Again, if we discuss in terms of supply, GST paid on inputs used for taxable supplies is eligible for credit but exempted supplies already enjoys 0% GST, hence ITC used for the purpose of exempted supplies cannot be claimed as it leads to negative taxation.

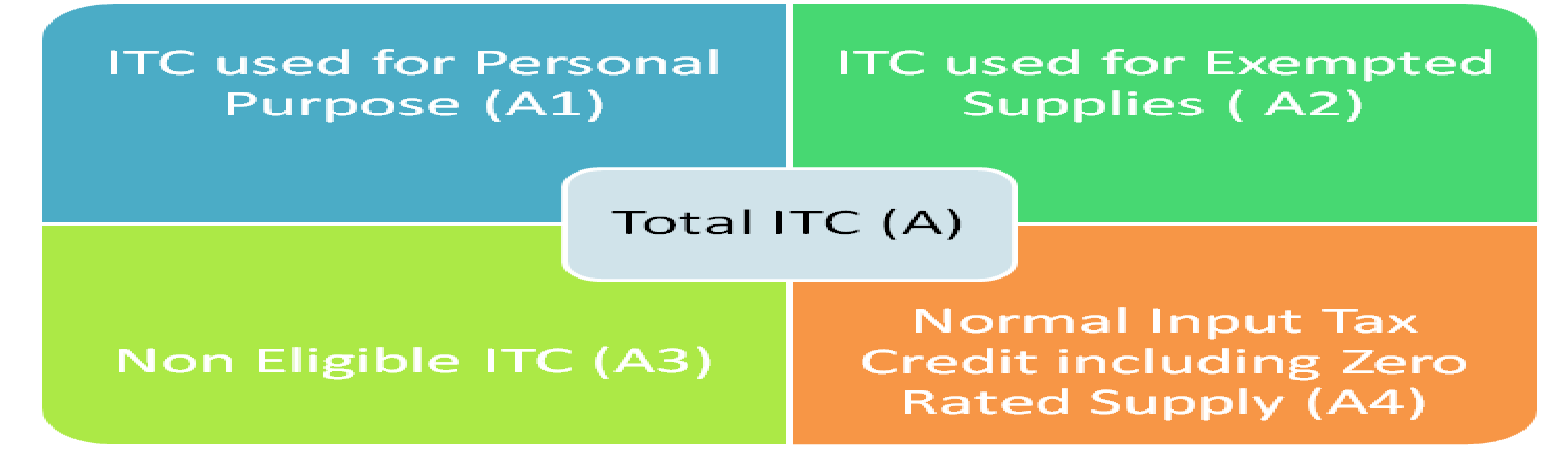

Types of ITC:

So, if we discuss it as a whole, for driving eligible ITC we need to remove ITC paid on personal expenses, exempted supplies and Non Taxable Supplies.

So, if we discuss it as a whole, for driving eligible ITC we need to remove ITC paid on personal expenses, exempted supplies and Non Taxable Supplies.

Calculating Common Credit:

Let us understand the calculation of common credit with the help of following example:

Figures for the month of Oct’19 are as follows:

Total ITC for the month of Oct’19= 1, 00,000 (A)

Sale Value of Taxable Supplies for the month of Oct’19 = 5, 00,000

Sale Value of Vegetable (Exempted Supplies) for the month of Oct’19=2, 00,000

Input Tax on Inputs used for personal purpose (eating out) =5,000 (A1)

Input Tax on Inputs used wholly for agriculture activities (Seeds, Soil etc.)=15,000 (A2)

Input tax on Inputs (Transporting Charges) used for wholly business purpose=18,000 (A4)

Input Tax on Input services on which availing ITC is not allowed (travelling by Uber to Whole seller)= 7,000 (A3)

With the help of above example we will try to understand that how to calculate the common credit and what will be the eligible credit which can be used for setting off output tax liability.

Mr. Vihaan Gupta is having following three types of ITC available with him:

Step -1 Finding out total eligible credit

Available Credit (C1)= Total ITC- (ITC for personal Expenses + ITC for Exempted Supplies + Non Eligible ITC)

= A-(A1+A2+A3)

=1,00,000-(5,000+15,000+7,000)

=73,000

With the help of this step, we calculate the eligible credit. Here Mr. Vihaan Gupta will have to reverse the ITC used for personal expenses, Exempted supplies and non eligible ITC in GSTR-2. So that it can be removed from the electronic credit ledger of taxpayer.

Step-2 Calculation of Common Credit

Common Credit (C2) = Available Credit (C1) – Normal Input Tax Credit (A4)

= 73,000-18,000

=55,000

This common credit includes credit for exempted supply, personal supply and normal supply. So common credit will be bifurcated among three and ITC related with exempted supply and personal supply will be reversed in GSTR-2.

So, there are three types of component in common credit:

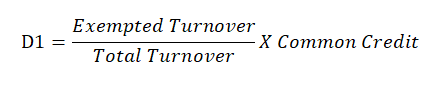

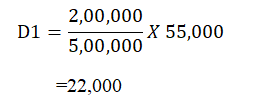

2.1 Partly Exempted

The portion of Exempted ITC can be calculated with the following formula:

So, as per our example,

The amount of exempted ITC is calculated using proportionate method. The amount of Rs. 22,000 is deemed to be credit pertaining with exempted supply, which will be reversed in GSTR-2.

2.2 Partly Personal

There are some expenses like rent, electricity, water bill etc. which are used for business and personal purpose both. This amount can be calculated by using the following formula.

D2= 5% of common credit

=55,000 X 5%

= 2,750

The above calculation is made by assuming that 5% is used for personal purpose. Here, this portion of personal ITC is required to be reversed in GSTR-2.

2.3 Normal Portion

Finally, we calculate the portion of ITC which pertains with normal supply, let’s do that:

D3= Common Credit (C2)-ITC portion for exempted supplies (D1)- ITC portion for personal expenses

= 55,000-22,000-2,750

= 30,250

This is the common credit attributable to normal supplies.

Step-3 In this step we will finally calculate amount of eligible credit.

Eligible Credit =30,250+18,000

= 48,250

Will Common credit reversal affect annual return?

In GSTR-2 format, you need to calculate the total ITC as per annual return. If there is a difference between the ITC as per annual return and the ITC claimed during the year, there will be a refund and interest as per the situation.

Now lets see different situation:

Situation 1- ITC claimed during the year 2017-18 is 2,00,000 but as per annual return it is 2,50,000

Here ITC claimed is less than ITC as per annual return, so additional ITC of Rs. 50,000 can be claimed till Sep of the following year.

Situation 2- ITC claimed during the year 2017-18 is 3,00,000 but as per

annual return it is 2,70,000

In this case ITC has been claimed in excess during the year 2017-18 by Rs. 30,000 which will be added in the output tax liability and taxpayer would also be required to pay interest @18% from 1st April,2018 till the date of payment.

So it is very much clear now that Input Tax credit rules are very much stringent and strict and needs to be followed very strictly.

The author of this article is CA Arti Agarwal, she is a practicing Chartered Accountant and a very prominent author of Efilingworld.

Message from Author: Hopefully you all understand this concept of Common Input Tax Credit very well, if you are having any problem regarding it, please feel free to call on 8126-416-416 or mail at info@efilingworld.com.