How to Calculate Aggregate Turnover in GST?

Do we require to get registered under GST? This is the question which came into the mind whenever you start or run any business or profession. So, the basic criteria for registration under GST are threshold limit. A business whose aggregate turnover exceeds Rs. 40 Lacs has to mandatorily register under GST. This limit is set to Rs. 20 Lacs for Special Category states. (This limit has been effective from 01.04.2019, earlier the limits were Rs. 20 Lacs and Rs. 10 Lacs for special category states.

For composition dealer, threshold limit is Rs. 1.5 cr. (with effect from 01.0.2019, earlier it was Rs. 1 cr.), in case of northern states and Uttrakhand threshold limit is Rs. 75 Lacs.

What is Aggregate Turnover?

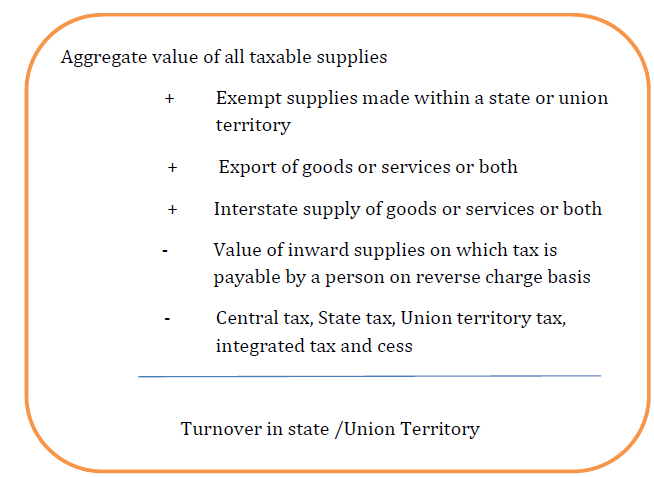

“Turnover in State” or “turnover in Union territory” means the aggregate value of all taxable supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis) and exempt supplies made within a State or Union territory by a taxable person, exports of goods or services or both and inter-State supplies of goods or services or both made from the State or Union territory by the said taxable person but excludes central tax, State tax, Union territory tax, integrated tax and Cess;

Calculation of Aggregate Turnover

Mr. Vihaan Gupta Owns a building in which he is running a vegetable shop, there is a plot adjacent to the shop which is also owned by Mr. Vihaan Gupta. On the plot he grows the vegetable and sells them in his shop. This activity is exempt under GST. Annual turnover of vegetables are Rs. 1.75 Cr., he provides plastic begs along with vegetable for which he is charging separately. His turnovers of the plastic bags are Rs. 7 Lacs. As we know, that sale of plastic bags is chargeable under GST. So if we will see then Taxable sale of Mr. Vihaan Gupta is Rs. 7 Lacs.

But if we analysis the above mentioned definition, exempt supplies are also included in the Aggregate Turnover. So, Aggregate in the above case will be Rs. 1.75 Cr, and since threshold limit for GST registration is Rs. 40 Lacs (w.e.f 01.04.2019), Mr. Vihaan Gupta is liable for GST registration. Though, he is not eligible for taking registration under Composition scheme, as his turnover exceeds the threshold limit of Rs. 1.5 Cr. (w.e.f. 01.04.2019).

Special Category under GST

Following are the states which has been the special category status under the Good and Service Tax:

- Arunachal Pradesh

- Assam

- Jammu & Kashmir

- Manipur

- Meghalaya

- Mizoram

- Nagaland

- Sikkim

- Tripura

- Himachal Pradesh

- Uttrakhand

The threshold limit for all the states are Rs. 20 Lacs ( w.e.f. 01.04.2019). So again if we will analysis the above example by modifying the figures:

Mr. Vihaan Gupta Owns a building in which he is running a vegetable shop, there is a plot adjacent to the shop which is also owned by Mr. Vihaan Gupta. On the plot he grows the vegetable and sells them in his shop. This activity is exempt under GST. Annual turnover of vegetables are Rs. 25 Lacs, he provides plastic begs along with vegetable for which he is charging separately. His turnovers of the plastic bags are Rs. 2 Lacs. As we know, that sale of plastic bags are chargeable under GST. So if we will see then Taxable sale of Mr. Vihaan Gupta is Rs. 2 Lacs.

But if we analysis the above mentioned definition, exempt supplies are also included in the Aggregate Turnover. So, Aggregate in the above case will be Rs. 25 Lacs, and since threshold limit for GST registration for special category states is Rs. 20 Lacs (w.e.f 01.04.2019), Mr. Vihaan Gupta is liable for GST registration.

The author of this article is CA Arti Agarwal, she is a practicing Chartered Accountant and a very prominent author of Efilingworld.

Message from Author: Hopefully you all understand this concept of Aggregate Turnover very well, if you are having any problem regarding it, please feel free to call on 8126-416-416 or mail at info@efilingworld.com.